Canadian Hydrogen Observatory: Insights to fuel…

Broker-Dealer Supervision Guide

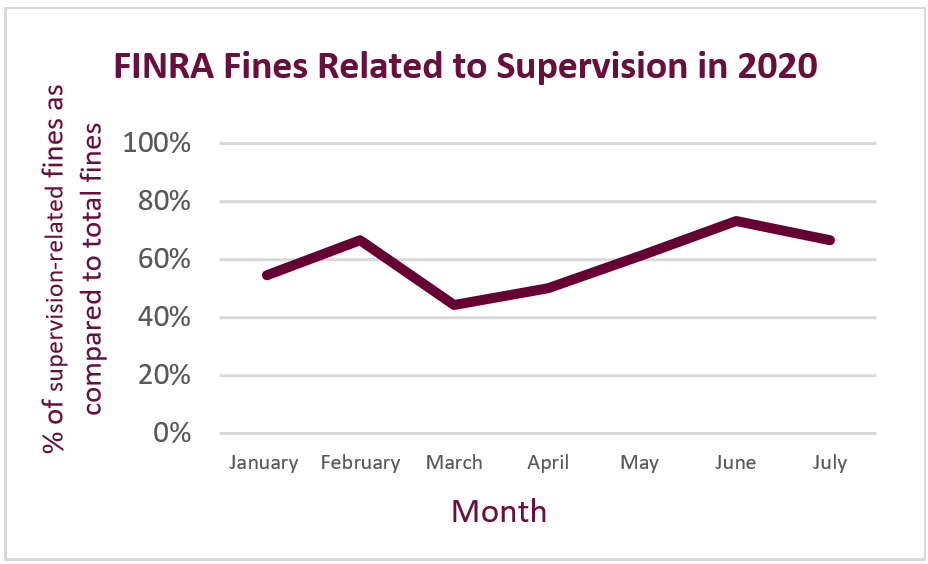

Broker-dealers are facing increased regulatory scrutiny regarding their supervisory programs. The Financial Industry Regulatory Authority (FINRA), which oversees U.S. broker-dealers, places high importance on supervision. During the first 7 months of 2020, FINRA has fined nearly 80 firms for non-compliance with securities rules and regulations. Over 60% of those total fines were related to supervision.

The following chart illustrates the percentage of FINRA fines imposed on firms that were related to supervisory deficiencies during the months of January 2020 – July 2020. Supervision related fines have never once fallen below 40% of total fines during this time period.

Source : FINRA Monthly Disciplinary Actions (2020)

In addition, FINRA’s 2019 Examination Findings Report, published in October 2019, opened with supervision related findings. At least a third of all findings discussed in the report were supervision related, across different areas of examined firms. Further, FINRA’s 2020 Risk Monitoring and Examination Priorities Letter, published in January 2020, highlighted issues of importance to FINRA's regulatory programs. Specifically, it described areas of focus for FINRA’s 2020 risk monitoring, surveillance and examination programs. Supervision was again highlighted as one of the top focus areas of FINRA’s exam program.

To add some additional context, below are a few recent high profile cases in which firms were fined for supervisory deficiencies:

This insight serves as a guide to helping you determine if your firm has an adequate supervisory system in place, just in time for FINRA’s 2021 examination program. We will discuss the FINRA rules related to supervision and then break down the specific requirements related to supervision of individuals and business practices. We will conclude by detailing a list of best practices to consider when developing, monitoring, or reviewing your firm’s supervisory system.

FINRA: America’s broker-dealer watchdog

FINRA is the largest regulator for all securities firms conducting business in the United States. The Securities and Exchange Commission (SEC) oversees FINRA’s operations. FINRA was founded in 2007 and is the successor of the National Association of Securities Dealers (NASD) and the member regulation, operations, and enforcement of the New York Stock Exchange (NYSE). FINRA is a private, Self-Regulatory Organization (SRO) and oversees all U.S. broker-dealers

FINRA Rule 3110 is intended to ensure that a firm establishes and maintains a system to adequately supervise the activities of its associated persons. The Rule requires that firms establish and enforce WSPs that are reasonably designed to supervise the activities of their associated persons and the types of businesses in which they engage. Per the rule, the WSPs should describe the specific individual(s) responsible for each review, the supervisory activities that such persons will perform, the frequency of the review, and the manner of documentation.

Many firms face challenges in meeting the requirements of this rule. Common issues that FINRA has observed include, but are not limited to, the following:

FINRA Rule 3120 is intended to ensure that firms implement Supervisory Control Policies (SPCs) that test and verify their supervisory procedures. This rule requires that firms not only have WSPs, but create SPCs to test and verify that their WSPs are adequate and reasonably designed to achieve compliance with applicable rules and regulations.

FINRA has observed that many firms face challenges in establishing SPCs that test and verify WSPs. One challenge is differentiating between WSPs and SPCs and understanding the requirements for establishing both policies. SPCs should be specifically designed to test and verify that a firm’s WSPs are adequate.

FINRA Rule 3130 requires firms to designate and identify to FINRA on schedule A or Form BD one or more principals to serve as a Chief Compliance Officer (CCO). The rules also require a firm’s Chief Executive Officer (CEO) to complete an annual certification, to certify that the firm has processes in place to establish, maintain, review, test and modify policies and procedures to achieve compliance with applicable rules and regulations.

FINRA has observed that a common occurrence among firms is their failure to have the CEO certify annually that the institution has processes in place to establish, maintain, review, test and modify written compliance policies and WSPs. Additionally, many firms fail to certify that the CEO has conducted one or more meetings with the CCO in the preceding 12 months to discuss such processes.

FINRA Rule 3270 requires that all registered individuals disclose their outside business activities (OBAs) to their employing broker-dealer. A business activity is any activity conducted outside of the firm where an individual is compensated or has a reasonable expectation of receiving compensation. Additionally, activities including acting as an employee, independent contractor, sole proprietor, officer, director, or partner of another entity, would be considered OBAs under the rules regardless of compensation factors. Some examples of OBAs can include, employment at an investment adviser, owner of a holding company, independent contractor, or even a part-time lacrosse coach.

The purpose of this rule is to be aware of all registered individuals’ activities in order to prevent conflicts from arising.

FINRA Rule 3270 requires that all registered individuals disclose their outside business activities (OBAs) to their employing broker-dealer. A business activity is any activity conducted outside of the firm where an individual is compensated or has a reasonable expectation of receiving compensation. Additionally, activities including acting as an employee, independent contractor, sole proprietor, officer, director, or partner of another entity, would be considered OBAs under the rules regardless of compensation factors. Some examples of OBAs can include, employment at an investment adviser, owner of a holding company, independent contractor, or even a part-time lacrosse coach.

The purpose of this rule is to be aware of all registered individuals’ activities in order to prevent conflicts from arising.

A Private Securities Transaction (PST) is a securities transaction made away from the firm. Per FINRA Rule 3280, if a registered individual participates in a PST and receives selling compensation, the individual must disclose the activity to the employing broker-dealer. The broker-dealer must supervise these transactions as if they are made on behalf of the firm. According to FINRA, selling compensation is defined as any compensation paid directly or indirectly from a source in connection with or as a result of the purchase or sale of a security.

Many firms have faced challenges in meeting the requirements of FINRA Rule 3270 and 3280. FINRA has published guidance on these rules, which discusses the following observed common issues identified during examinations:

FINRA Rule 3210 requires that all associated persons disclose their outside brokerage accounts to their employing broker-dealer. The employing broker-dealer must request transmission of duplicate copies of confirmations and statements, or transactional data from the firm executing the transactions.

Failing to establish an adequate system to review statements or activity can lead to employees committing fraudulent trading activities, such as insider trading, without the firm’s awareness.

Under FINRA Rule 3110, member firms are required to establish WSPs that detail the firm’s process for review of incoming and outgoing written and/or electronic correspondence. The supervisory procedures must be appropriate for the firm’s business size, structure, and customers.

The WSPs must also designate an individual to review the correspondence and such reviews must be evidenced in writing.

Failing to review incoming and outgoing correspondence can result in missing critical information such as customer complaints, unsuitable recommendations, unauthorized trading, churning, insider trading or other fraudulent and / or high-risk activity.

FINRA Rule 2111 describes the suitability obligations for member firms. According to FINRA, firms are required to have a reasonable basis to believe a recommended transaction or investment strategy involving a security or securities is suitable for a customer. There are three main suitability obligations for firms described below:

Per FINRA’s Regulatory Notice 20-18, FINRA has amended its Suitability Rule to address potential contradictions or overlaps with SEC’s Regulation Best Interest (Reg BI). These changes have become effective as of June 30th, 2020, which is the effective date of Reg BI. Specifically, FINRA has amended FINRA Rule 2111 to note that the rule will not apply to customer recommendations subject to Reg BI, in order to avoid duplication of efforts. Additionally, FINRA has removed the “element of control” from the quantitative suitability obligation in order to be consistent with Reg BI.

Under FINRA Rule 3110, member firms must detail in their WSPs, a process for review of securities transactions that is reasonably deigned to identify trades that may violate the provisions of the Exchange Act or FINRA rules prohibiting insider trading and manipulative and deceptive schemes.

Failure to identify such trades can directly impact customers, which could result in large fines. For example, as mentioned in the introduction of this paper, this past July, a firm was fined $700,000 for failing to establish a reasonable supervisory system to govern OTC trading activity. This led to instances where the firm traded ahead for its own account and executed prices that were not in its customers’ favor.

A firm that engages in Regulation D offerings must have supervisory procedures that are reasonably designed to ensure that each offering is properly supervised before it is marketed to other firms or sold directly to customers.

Additionally, FINRA requires that firms demonstrate reasonable due diligence investigation through documentation. FINRA’s Notice to Members 10-22 states that member firms should retain records documenting both the process and results of its investigation. Such records can include descriptions of the meetings that were conducted during the investigation. These descriptions can include meetings with the issuer or other parties, tasks performed, the documents and other information reviewed, the results of such reviews, the date of such events occurred, and the individuals who attended the meetings or conducted the reviews.

Many firms have faced challenges in meeting their due diligence requirements. FINRA has observed the following common issues during examinations:

Under FINRA Rule 3110, member firms are required to inspect annually every Office of Supervisory Jurisdiction (OSJ) and any branch office that supervises one or more non-branch locations.

Within FINRA’s Rule 3110 guidance, FINRA published the following common issues identified during examinations:

Sia Partners’ talent pool consists of former FINRA examination staff, with nearly 15 years of combined experience examining all types of U.S. broker-dealers. Leveraging our experience in this field, we have developed the following list of best practices to help your firm mitigate the risk of supervisory failures.

Zoya Ashirov

Senior Manager

917-330-5536

Zoya.Ashirov@sia-partners.com

Liana Marzano

Senior Consultant

732-403-4167

Liana.Marzano@sia-partners.com