Canadian Hydrogen Observatory: Insights to fuel…

A Market update on where Regulators and Industry Participants stand regarding ESG reporting and disclosure regulations in the US. The main focus is on recent comments and announcements from regulators such as SEC & FRB with an analysis of market participants' sentiments.

In this article, we provide a market update on recent developments specific to ESG reporting and disclosure regulations in the US. Our main focus was on the recent comments and announcements from U.S. regulators such as the SEC and FRB specific to anticipated regulatory changes surrounding ESG reporting and disclosures. We analyzed the financial services industry sentiment on stricter regulatory requirements from current clients and open comments provided via Open Comments in response to the SEC proposed rulemaking on ESG disclosures. We also provided background on existing frameworks from which US regulators may draw from in rule drafting. We conclude this article by sharing insight into how Sia Partners recommends financial services prepare for anticipated stricter ESG reporting and disclosure regulations, etc.

“Now more than ever, investors are considering climate-related issues when making their investment decisions. It is our responsibility to ensure that they have access to material information when planning for their financial future.” – S.E.C. Acting Chair Allison Herren Lee

The use of environmental, social, and governance (ESG) factors in investment analysis has grown rapidly over the past decade. Recent statistics from the OECD reveal that the amount of professionally managed portfolios with integrated key elements of ESG assessments now exceeds USD 17.5 trillion globally. Also, the growth of ESG-related traded investment products available to institutional and retail investors exceeds USD 1 trillion and continues to grow quickly across major financial markets. While ESG data played a more informal role in the investment process before, a more systematic approach to ESG integration is now becoming invaluable. However, the ESG investments ecosystem is still relatively a new concept. The complexity of measuring ESG performance due to issues such as greenwashing (fraudulent claims that deceive investors into believing that a company's products are environmentally friendly) and a lack of common ESG standards has investors and investment professionals calling for more guidance on ‘what’ is green. That is why financial regulators globally are developing various guides, regulations, and standards with ESG as the central theme, aiming to certify and promote ESG integration into the investment process. An example of such regulations is the development of a national green taxonomy by regulators who seek to “green” their countries financial systems.

The EU’s green taxonomy is starting to provide the first standardized classification tool for sustainable investments which will strengthen ESG practices in Europe, which may also pave the road for other initiatives globally and help combat greenwashing. Meanwhile, Canada’s Transition Taxonomy will complement the EU’s green taxonomy and support Canada’s transition to more sustainable business practices and to a net-zero carbon economy by 2050.

For Canadian investors and investment managers, the most impactful recent policy developments on sustainable investments would be the EU taxonomy for sustainable activities (also called green taxonomy) adopted by the European Commission earlier last year and the Canadian Transition Taxonomy that is in its cusps of being published by the Canadian Standards Association. CSA Group’s Technical Committee for Transition Finance

The United States is lagging behind both the EU and Canada when it comes to reporting ESG disclosures, leaving businesses unaware of how to disclose information about their climate-related risks in a digestible way to stakeholders. As investors and customer’s behavior is changing, the demand for standard reporting is increasing. SEC Acting Chair Allison Lee has announced that the SEC is in the process of developing a “comprehensive framework that produces consistent, comparable and reliable climate-related disclosures”. In her public statement, she created an open comments period to discuss advantages and disadvantages of the TCFD, CDSB, and SASB frameworks . These frameworks are described in detail below.

The SEC Public Statement on Climate Change Disclosures listed three main disclosures frameworks for consideration: The Taskforce on Climate-Related Disclosures (TCFD), Climate Disclosures Standards Boards (CDSB), and Sustainability Accounting Standards Boards (SASB). The below table summarizes the objectives, global scope, background, and high-level details into the methodology of the disclosure framework

| Taskforce for Climate-Related Disclosures (TCFD) | Climate Disclosures Standards Boards (CDSB) | Sustainability Accounting Standards Boards (SASB) | |

|---|---|---|---|

| Objective | Industry-led initiative created to develop a set of recommendations for voluntary climate-related financial disclosures | To promote and advance climate change-related disclosure in a mainstream report through the development of a global framework | To develop standards for use in corporate filings to the U.S Securities and Exchange Commission (SEC), so investors can have comparable of non-financial. |

| Scope | Established in 2015 by the Financial Stability Board (FSB). SCope of over 1000 supporters globally as of 2020 | Established in 2007 by the World Economic Forum (WEF). Scope usage by over 300 companies, 32 countries across 10 sectors as of 2017 | Established in 2011. Scope covers over 598 reporters and 727 mentions in 2021 |

| Background | The TCFD has developed recommendations for companies to focus on to create more transparent disclosures around climate-related issues. When following these recommendations, stakeholders are more informed around their investment, credit and insurance underwriting decisions | The CDSB provides companies with a framework for reporting environmental and climate change related information that complements already existing financial reporting. It allows companies to provide investors with environmental information through a standard corporate report to aid in decision making. | SASB developed these standards in order to answer the increasing demand from investors are allowed to compare performance on critical ESG issues within an industry |

| Methodology | Disclosures recommendations structured around four thematic areas that represent core elements of how organizations operate: Governance, Strategy, Risk Management, Metrics & Targets | 12 reporting requirements while aligning with TCFD elements include: Governance, Management's environmental policies, strategy & targets, Risks and opportunities, Sources of environmental impact, Performance and comparative analysis, Outlook, Organizational boundary, Reporting policies, Reporting period, Restatements, Conformance, and Assurance | Available for 77 industries internationally. Companies are rated according to five ESG dimensions: Environment, Social Capital. Human Capital, Business Model & Innovation, and Leadership & Governance |

A major announcement at the Glasgow COP26 summit was the International Sustainability Standards Board (ISSB), from the International Financial Reporting Standards Foundation. The ISSB is a consolidation of the Value Reporting Foundation (consisting of the Sustainability Accounting Standards Board and International Integrated Reporting Council), and Climate Disclosure Standards Board. The ISSB is working to align with progress towards focus on standardized regulation and monitoring of climate risk at a global level. Specifically, the ISSB is set out to develop a comprehensive global baseline of high-quality sustainability disclosure standards to meet investors’ information needs. From a U.S. perspective, Allison Lee has commented that the SEC, through IOSCO and other international work streams, is involved in the efforts of the ISSB and hopes to use their guidelines as a baseline for the Commission’s climate disclosure proposal. The SEC is working intimately with the comments received in the open comments period and has announced there will be another open comments period, once a proposal has been made, for the public to react to the specifics and help inform any final rule.

Methodology

To better understand the industry’s response to the SEC’s Public Statement’s request for comments for the design of climate related disclosures regulations, our US Sia Partners team (a) leveraged our banking expertise and client network in our 10 US locations and (b) conducted a literature review of the open comments feedback. From our engagement with the industry and analysis of the open comments feedback, we have identified some trends which would reflect the future design, implementation, and challenges of an SEC regulated climate-related disclosure.

Public Input on the Design of SEC Climate Change Disclosures

Although each type of responder had included nuances in the comments and there was no unanimous framework for the future-state of SEC climate related disclosures there were some significant common trends among the significant market players that responded. Below are some of the trends identified in the comments regarding the design, implementation, and challenges of future SEC Climate Change disclosures.

Design

Implementation and Challenges

Given the SEC’s increasing focus on climate-related disclosures, it is important for financial institutions to be prepared for potential stricter disclosures requirements and regulatory scrutiny. The preparatory steps highlighted below are just a small sample of the key activities organizations should be conducting as they prepare for U.S. regulatory changes.

Educate

Govern

Assess

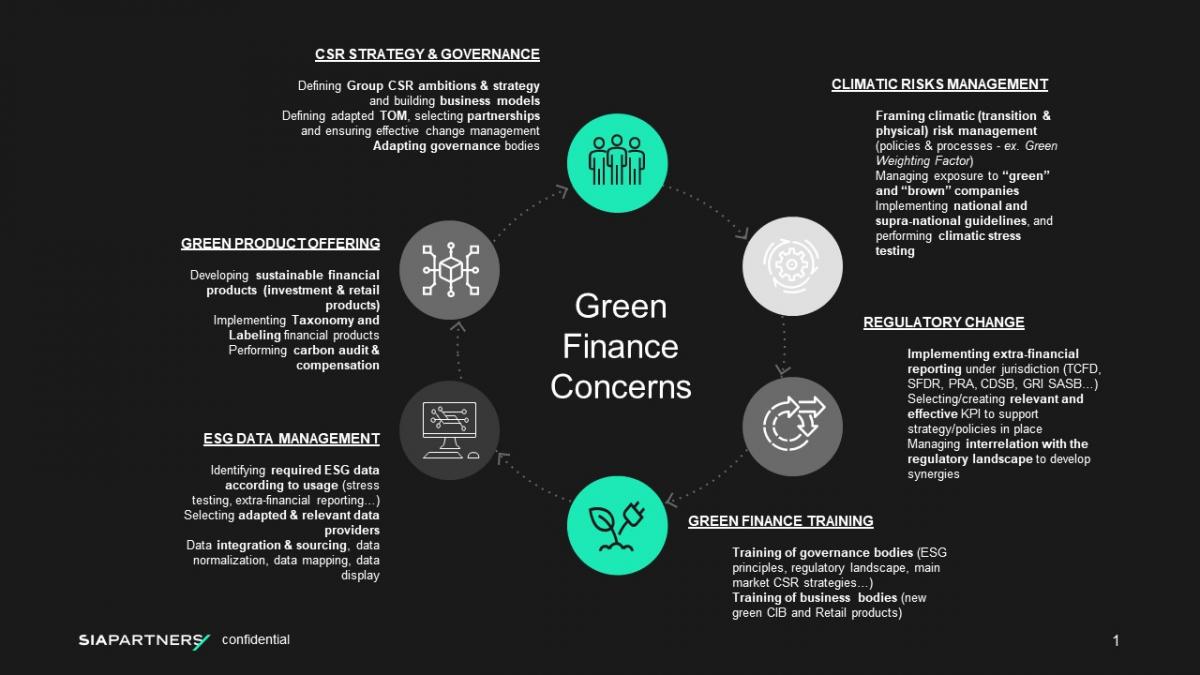

Adapting to new disclosure requirements and integrating these new standards within your company’s current reporting processes will require strategic planning and transformation. Sia Partners brings perspective from decades of experience helping companies transform their organization to comply with new and rapidly evolving regulatory requirements. In addition, Sia Partners is well positioned to support the emerging challenges associated with ESG due to our deep ESG and climate expertise through our Climate Analysis Lab.

From Strategy to Operations, Sia Partners capabilities in Green Finance and Climate Risk can help organizations prepare and implement the necessary organizational changes to comply with stricter requirements from U.S. Regulators.

To learn more about how Sia Partners could help your organization address regulatory change associated with ESG and climate risk disclosures, please reach out to our ESG and climate risk focused consultants using the form below