Canadian Hydrogen Observatory: Insights to fuel…

Global Oil Supply Squeeze Spikes Prices and an Ongoing Resilience of the European Gas Market

| 2022 | 23Q1 | 23Q2 | 23Q3 | 23Q4*** | 24Q1*** | ||

|---|---|---|---|---|---|---|---|

| Crude Prices* | Brent ($/bbl) | 100.78 | 81.17 | 78.32 | 87.5 | 90.67 | 94.67 |

| Rig Count*** | World | 1834 | 1900 | 1797 | 1760 | - | - |

| Consumption (mb/d)* | Total | 99.8 | 100.1 | 100.8 | 101.4 | 101.7 | 101.7 |

| OECD | 46.0 | 45.3 | 45.4 | 46.0 | 46.3 | 45.5 | |

| non-OECD | 53.8 | 54.7 | 55.4 | 55.4 | 55.4 | 56.2 | |

| Production (mb/d)* | Total | 101.0 | 101.0 | 101.0 | 101.1 | 101.6 | 101.5 |

| OPEC | 34.4 | 34.4 | 33.7 | 32.7 | 32.9 | 33.1 | |

| non-OPEC | 66.6 | 67.1 | 67.4 | 68.4 | 68.7 | 68.4 | |

| Excess (+) / Deficit (-) | 1.2 | 0.9 | 0 | -0.3 | -0.1 | -0.2 |

This third quarter was marked by a significant increase in oil prices which have risen by 28%, ranging between $70-$80/barrel all year and reaching $90/barrel this quarter, its highest value since mid-November 2022. This upturn can be attributed to various factors, including the positive shift in the macroeconomic sentiment with the ease of inflation and OPEC+'s announcement of new production cuts, as well as the extension of Saudi Arabia and Russia’s voluntary export production cuts until the end of 2023 despite the potential uptick in demand for oil products typically witnessed in the final trimester. This uptrend in prices is expected to persist in the near term.

| Location | Average price Q3 | December Future | January Future | February Future |

|---|---|---|---|---|

| Henry Hub (US) [$/MMBtu] | 2.59 | 3.56 | 3.85 | 3.78 |

| TTF (Europe) [€/MWh] | 32.23 | 48.56 | 50.32 | 50.84 |

| JKM (Asia) [$/MMBtu] | 12.66 | 17.65 | 17.08 | 17.23 |

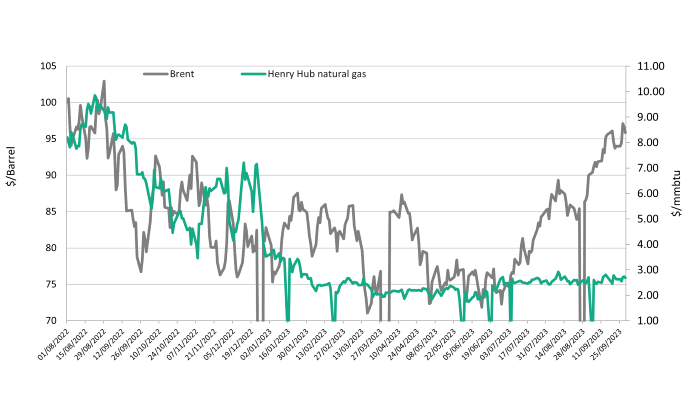

In Q3 2023, gas markets experienced heightened volatility, notably in the European benchmark (TTF month-ahead contract), reaching its highest level since Russia's invasion of Ukraine. Strike risks in Australia and outages in Norway raised concerns for near-term gas supply. European storage sites opened the 2023-2024 heating season at 96% of total capacity and 10 bcm above their five-year average. In the North American gas market, Henry Hub gas prices have declined significantly (~22.0%) since the start of the year, despite a prolonged heat wave in the south of the U.S. driving strong regional demand for natural gas during the summer due to a combination of a relatively mild winter and temporary partial closure of the Freeport LNG terminal that resulted in rising U.S. storage inventories. In fact, as of September 22, 2023, U.S. gas inventories stood at 3.3 Tcf. In the Asia Pacific, gas demand grew moderately during Q2-Q3 2023. Despite the increasing gas consumption in China and select emerging Asian markets, gas demand continued to be subdued in the region's mature markets due to the enhanced availability of nuclear energy. Projections indicate that Asian gas demand is anticipated to grow by 3% in 2023, with robust support from the power and industrial sectors.

Brent Oil & Henry Hub Natural Gas Prices – Data source: EIA Short-Term Energy Outlook October 2023 database

OPEC+ Countries Ongoing Reliance on Production Cuts as Key Strategy to Control the Market

Crude oil prices have been navigating a turbulent path this year, influenced by many fundamental factors that shape the intricate dynamics of the global oil trade. Central to this narrative is the role played by OPEC+ in steering the trajectory of oil prices with the implementation of production cuts since 2022, which were frequently extended. In June of this year, the alliance decided to limit combined oil production to 40.463 million barrels per day over January- December 2024. This strategic decision underscores the alliance's unwavering commitment to maintaining a certain level of oil prices, offering traders a foundational assurance that there are limits to how far prices will decline.

This quarter is a testament to the alliance's collective effort to fortify the market. Notably, Saudi Arabia and Russia, key players in the OPEC+ alliance, implemented voluntary cuts of 1 million barrels per day (bpd) and 300,000 bpd, respectively, in July, which kept the alliance’s output below levels earlier this summer with Saudi Arabia's crude production reaching its lowest point since May 2021. These restraints have been a significant factor behind the recent rise in crude prices to 10-month highs. Furthermore, the two countries jointly announced on Sept. 5th the extension of their production cuts through the end of 2023 while remaining ready to consider either deepening cuts or raising output based on evolving market conditions.

However, this impact was tempered by output increases in Iran, Iraq, and Nigeria. Iran’s August oil production was the highest since November 2018 as its exports to China remain strong and sanctions pressure easing considerably as Western countries focus on measures against Russia in response to its invasion of Ukraine. This enabled customers to take more Iranian crude without fear of enforcement. The output curbs by OPEC+ members have also been offset by higher supplies from producers outside the alliance, primarily the U.S., which has urged OPEC+ to raise output to secure lower energy costs and help the global economy. A call that was also backed by the US’s Western allies. Nevertheless, OPEC+ producers argue they are acting to maintain market stability and are pre-emptive with abundant money-printing by Western central banks over the past decade, dampening the value of their main export product, which accounts for a large share of their revenue.

The ongoing saga of crude oil prices, shaped by OPEC+ cuts, underscores the intricate and interconnected nature of global oil markets. As these geopolitical and economic forces continue to play out, market participants and observers alike will keenly watch for further developments that could sway the delicate balance of supply and demand, ultimately influencing the direction of oil prices in the upcoming months.

A Focus on China: Oil Imports Boom and the Looming Shifts in Global Energy Dynamics

China’s heavy oil import recovery has been closely watched since the reversal of the country’s zero-COVID policy and the reopening of the economy at the end of 2022.

Indeed, China’s crude oil imports reached record volumes during the first half of 2023, averaging 11.4 million barrels per day (b/d), a substantial 12% increase from the 2022 annual average of 10.2 million b/d. Key suppliers were Russia, Iran, Brazil, and the United States, with notable increases in imports from Russia by 23% (400,000 b/d), Saudi Arabia by 7% (130,000 b/d), and Brazil by an impressive 49% (250,000 b/d) compared with 2022 averages. Notably, China imported a staggering 2.6 million b/d of crude oil from Russia in June alone, a historic high for any country in any given month. Moreover, China's imports from the United States more than doubled in the first half of 2023 compared to 2022.

Additionally, the General Administration of Customs reported that Chinese refiners processed a record 14.7 million b/d of crude oil in the first half of 2023, showcasing an 8% increase from the 2022 annual average of 13.5 million b/d and surpassing China's previous record set in 2021. This notable increase in crude oil processing can be attributed, in part, to the introduction of new refinery capacity. Noteworthy among these are the 320,000-b/d Shenghong Petrochemical refinery in Lianyungang, operational since November 2022, and the 400,000-b/d PetroChina Jieyang refinery, which commenced trial runs in February 2023.

However, the heavy dependence of oil markets on China presents a looming threat. Speculation abounds that China's oil demand is approaching its peak, with projections suggesting a plateau within three to five years. This potential shift is argued by China's intensified efforts toward energy transition to reach carbon neutrality by 2060 and peak the country’s carbon emissions by the end of 2030. The concerns regarding the sustainability of the current oil market dynamics further arise as general economic growth in China slows in the longer term. On the other hand, India is set to overtake China as the largest oil demand growth center toward the end of the decade and make up, with Southeast Asia, for the void left by China's potential decline in crude demand. India’s economy grew 7.8% in the second quarter of this year, marking the fastest pace of growth in a year. The country is also widely expected to become the third-largest economy by 2030.

Global Gas Landscape Shifts: Gas Projects, Emerging Markets, and the Imperative of Carbon Capture

The global gas landscape has witnessed significant developments in 2023, marked by Iran’s inauguration of the last phase of the “South Pars/North Dome” in August. This field, situated in the Persian Gulf and jointly owned by Iran and Qatar, is the world's largest natural gas field. This milestone comes amidst a flurry of gas projects worldwide, including ventures by Perenco in Gabon, TotalEnergies in Mozambique, Qilak in Alaska, and Cheniere in Louisiana. Moreover, the gas market’s dynamics are further shifting as countries like Iraq aim to reduce reliance on gas imports by expanding gas concession areas for foreign companies. The Philippines, emerging as a frontier LNG market, has also captured the attention of global LNG producers and traders.

Against this backdrop, industry leaders convened at Gastech 2023, the world's largest exhibition and conference for natural gas, LNG, hydrogen, low-carbon solutions, and climate technologies. Held in Singapore, the event brought together market players, policy analysts, investors, and technology innovators. Central to discussions were emissions reduction technologies, with a particular focus on methane emissions, known to be over 25 times more potent at trapping atmospheric heat than CO2. The spotlight of this edition was mainly put on carbon capture and storage (CCS) and its potential to revolutionize global capabilities, which are further highlighted in our last Oil & Gas Insights (Oil & Gas Q2 2023 Insights: A Shifting Landscape (sia-partners.com). It is, however, crucial to note that Europe and the U.S. were on track to sequester only 1.5-2.0% of their current emissions by 2030 last year, as revealed by the Global CCS Institute. This falls short of the requirements to meet the 1.5°C pathway by 2035, emphasizing the urgent need for accelerated efforts in adopting CCS technologies. On the other hand, the Chief Executive Officer of the Asia Natural Gas & Energy Association (ANGEA) emphasized the pivotal role of natural gas and carbon capture in Asia's energy transition. Particularly for heavily emitting North Asian countries, these technologies are deemed indispensable. The intricate balance between meeting energy demands and mitigating environmental impact necessitates a comprehensive approach to integrating natural gas and robust carbon capture strategies.

As the global energy landscape continues to evolve, the intersection of gas projects, emerging LNG markets, and the imperative for emissions reduction technologies are shaping the industry's trajectory. The challenges highlighted at Gastech 2023 and the urgent need for effective carbon capture and storage solutions underscore the critical juncture the world finds itself in pursuing a sustainable and resilient energy future. The collaboration of industry stakeholders, policymakers, and innovators will be crucial in navigating this complex landscape and ensuring a successful transition toward a low-carbon paradigm.

An evolving European gas market to mitigate potential risks of gas supply disruptions ahead of the upcoming winter season

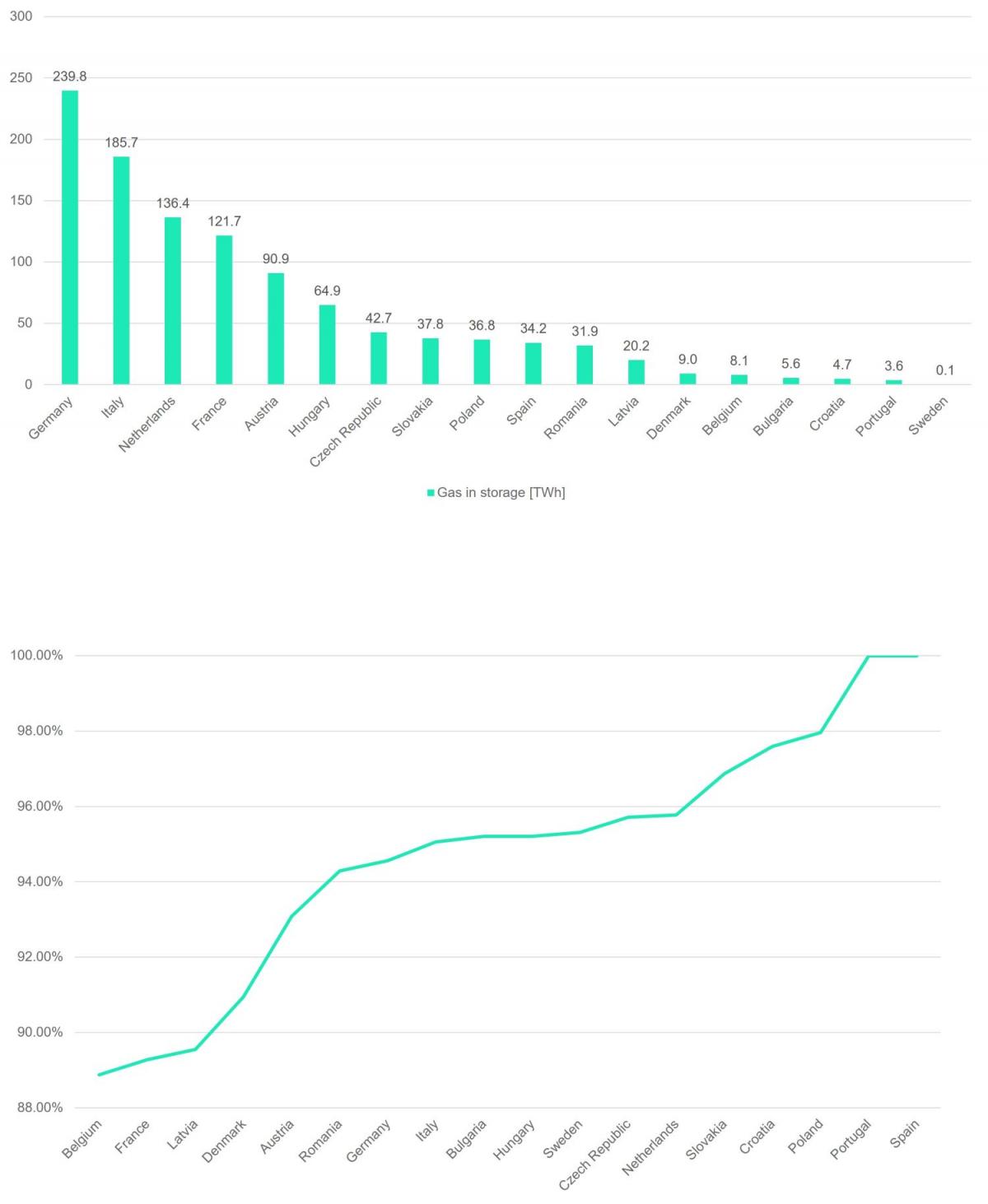

The European natural gas market is shaped by various factors, including the decline in gas prices and the European Union's commitment to achieving a storage capacity of 90% by November 1st annually, as mandated by the gas storage regulation established in June 2022. The European storage level will reach 1024 TWh, equivalent to just over 93 billion cubic meters (bcm). While this storage objective has been met in nearly every European country during Q3 2023, exceptions include Latvia, France, and Belgium, each exhibiting varying volumes, as illustrated in the figures below.

European countries gas storage (above), Current stock filling % in European countries (beneath)

Thus, the European market remains very volatile, mainly influenced by an embargo on its gas exports with the implementation of sanctions against Russia. The Russian share in the European natural gas trade has decreased by 21% in a year, going from 39% of total European natural gas imports by pipeline in Q1 2022 to 17.4% in the same quarter of this year. On the flip side, European countries have sought to broaden their sources of imports by establishing agreements with new partners. The EU recorded a cumulative import of 94.73 million metric tons in 2022, a significant increase from the 57.27 million metric tons imported throughout the entirety of 2021, with a substantial portion of the imported natural gas sourced from the United States and Qatar, which presented respectively 40% and 13% of total imports in Q1 2023.

As observed throughout this quarter, the European market remains susceptible to volatility due to workers' strikes at Chevron's LNG facilities in Australia, which heightened fluctuations in spot gas prices. Notably, the day following the announcement of the strike, the Dutch FTT (regarded as the European benchmark) surged by nearly 9.5%. While this impact is anticipated to be temporary, it underscores the ongoing challenges within the market.

In the wake of the Ukrainian war's onset, oil and gas companies find themselves at a critical juncture, compelled to reassess their operations in Russia. The financial ramifications of disengagement are substantial, exemplified by BP's estimated loss of over 22 billion euros after its withdrawal in February 2022. Yet, staying in the country presents challenges entangled in legal and political uncertainties while incurring significant reputational costs amid US and EU sanctions.

Russia's diminished buyer base, a consequence of sanctions and embargoes, has led the country to seek alternative consumers. India and China have emerged as primary purchasers since European interventions, prompting Russia to explore new markets, including Brazil, where its first crude oil cargo is set to be exported this September.

While geopolitics influences the decisions of oil and gas firms, it is not the sole driving factor. The energy transition looms large on the industry's horizon, with the International Energy Agency (IEA) predicting a peak in oil, natural gas, and coal demand before 2030. The IEA's head, Fatih Birol, called the situation the "beginning of the end" for oil and gas. Today, “new large-scale fossil fuel projects carry not only major climate risks but major financial risks” he said.

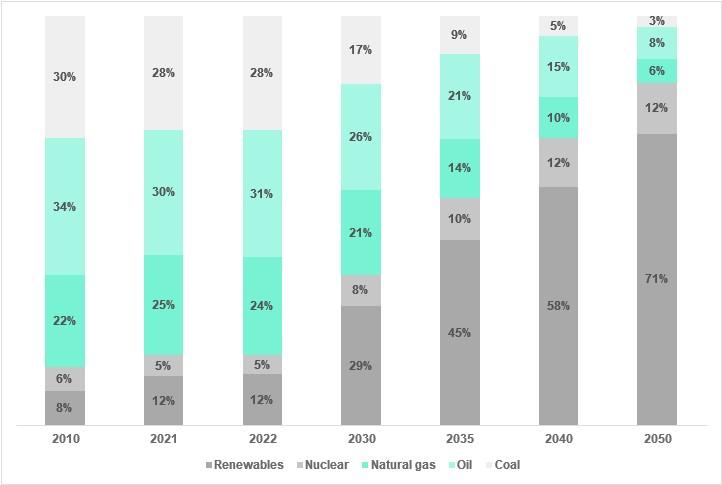

Evolution of the place of oil and gas in the world energy supply – Data source: IEA (2023)

Some industry leaders, like BP and Saudi Aramco, are redirecting investments toward low-carbon solutions, with BP planning to allocate 40% of its annual capital expenditure to "transition growth engines" by 2025. Large-scale projects in low-carbon fuels, renewables, and electric vehicle (EV) charging are becoming focal points for diversification, with BP committing up to 10 billion euros in such ventures in Germany by the decade's end. The United Arab Emirates has similarly pledged a $4.5 billion investment in clean energy in Africa, targeting 15 GW of clean energy by 2030.

However, despite these diversification efforts, oil and gas players show no signs of slowing down their historical activities. Iraq, for instance, expressed its intention in August 2023 to expand oil and gas concession regions, aiming to utilize its gas supplies for domestic facilities and reduce dependency on imports, primarily from Iran. Similar sentiments are echoed in some occidental countries, such as the United Kingdom, which approved "at least 100" oil and gas licenses in the North Sea, drawing criticism from environmental groups.

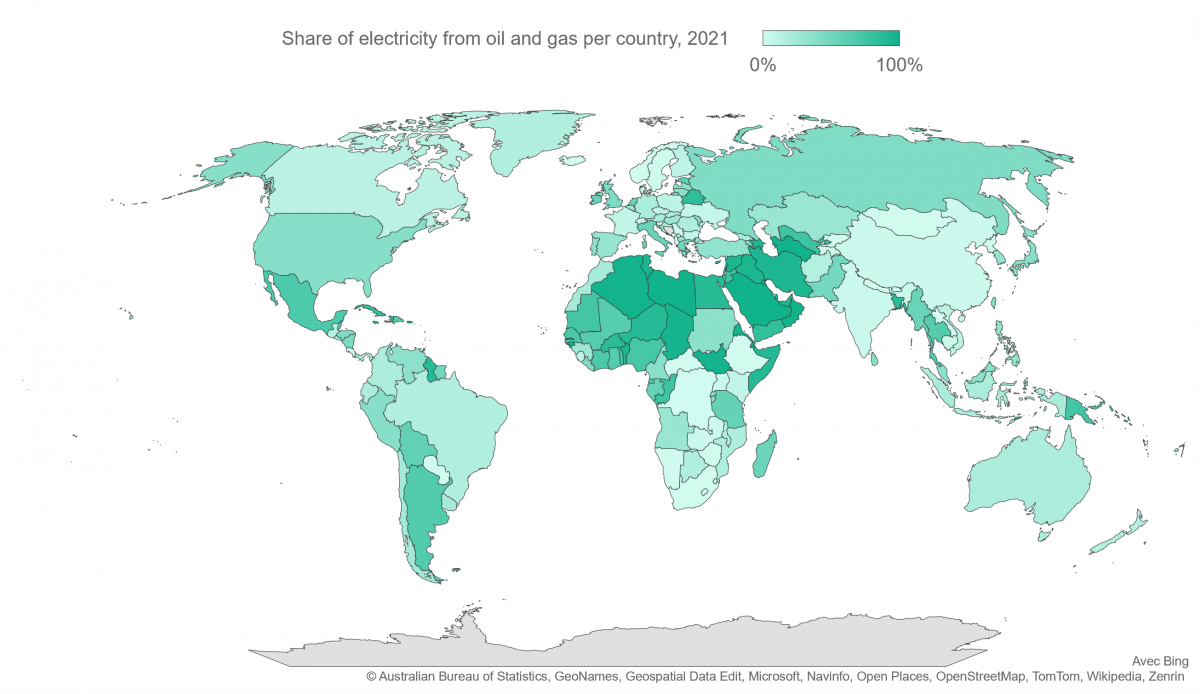

Variation in the proportion of oil and gas used in a country's electricity mix – Data source: OurWorldInData (2023)

As the industry grapples with varied strategies and approaches, the looming COP 28, scheduled for November 30 to December 12 in Dubai, becomes a focal point. Chaired by Sultan Al Jaber, CEO of the Abu Dhabi National Oil Company (ADNOC) and United Arab Emirates Minister of Industry and Advanced Technology, COP 28 anticipates crucial debates among stakeholders. France has unveiled its oil phase-out strategy and encourages neighboring countries to follow suit. However, the industry insists on the necessity of operating oil wells as long as demand persists.

The contradictory landscape presents challenges in making decisions aligned with shared objectives, and all eyes are on COP 28 for potential resolutions to the complex web of geopolitical, environmental, and economic challenges facing the global oil and gas industry.