Canadian Hydrogen Observatory: Insights to fuel…

Discover Sia Partners' oil and gas insights, including uncertainties driven by Russia and China, prompting a surge in mergers and acquisitions (M&A).

The oil and gas dynamics were driven by a combination of factors during the first quarter of 2023, including the recovery of Chinese demand, EU sanctions and price caps on Russian oil and gas product exports, a mild winter in the Northern Hemisphere, and geopolitical tensions in key producing regions. These factors created a volatile and dynamic market environment during this period.

| 22Q2 | 22Q3 | 22Q4 | 2022 | 23Q1** | 23Q2** | ||

|---|---|---|---|---|---|---|---|

| Crude Prices | Brent ($/bbl)* | 108,7 | 93,2 | 82,8 | 94,8 | 81,07 | 78,0 |

| Rig Count | World | 1706 | 1853 | 1834 | 1834 | 1879*** | - |

| Deland (mb/d) | Total | 98,8 | 100,8 | 100,8 | 100,0 | 100,3 | 101,3 |

| OECD | 45,4 | 46,6 | 46,0 | 46,0 | 46,0 | 45,9 | |

| non-OECD | 53,4 | 54,1 | 54,8 | 54,0 | 54,3 | 55,4 | |

| Supply | Total | 98,8 | 101,1 | 101,3 | 100,0 | 101,2 | 101,3 |

| OPEP | 28,8 | 29,5 | 29,4 | 20,0 | 29,3 | 29,4 | |

| non-OPEP | 64,8 | 66,2 | 66,6 | 65,7 | 66,7 | 66,9 | |

| Excess (+) / Deficit (-) | 0,0 | 0,3 | 0,5 | 0,0 | 0,9 | 0,3 |

*Source: EIA (U.S. Energy Information Administration) March 20th

**Source: IEA (International Energy Agency) projections 20/0

*** Total World Rig count in March 2023

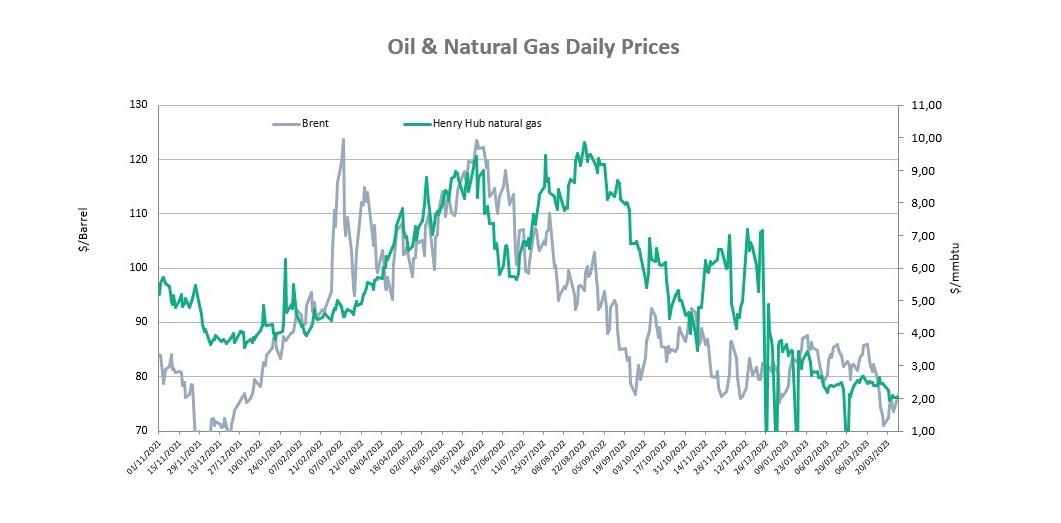

In January 2023, Brent oil prices dropped to pre-war levels, averaging $81 per barrel and experienced a slight decline in February of approximately $1 per barrel, with trading remaining range bound. The price drop was attributed to waning confidence in China's reopening and a hawkish shift in central bank policies. By March, prices had fallen further, declining by $3 per barrel due to growing macroeconomic concerns in response to the collapse of Silicon Valley Bank. Despite these declines, oil supply was abundant during the first quarter of 2023, and shall continue into the second quarter, according to IEA projections. Despite this secure standing, the IEA predicts that China's increasing oil demand could lead world oil demand to record levels and potentially reverse the situation in the second half of the year, especially with the strict enforcement of supply ceilings by OPEC+.

| Location | Spot Price 31/03 | May Future* | June Future* | July Future* |

|---|---|---|---|---|

| Henry Hub (US) [$/mmbtu] | 2,1 | 2,38 | 2,52 | 2,71 |

| TTF (Europe) [€/MWh] | 46,61 | 42,4 | 42,65 | 43,25 |

| JKM (Asia) [$/mmbtu] | 13,51 | 12,59 | 12,85 | 13,79 |

Source: ICE Index, gas futures

*As of April 18th, 23, 3:59 PM (GMT)

Henry Hub, natural gas spot prices, saw historically low averages during the first quarter of 2023 after unseasonably warm weather, bringing the overall US gas demand down. The average European natural gas benchmark TTF price was €79.16/MWh during the same period showing a 16% decline over Q1 2022 due to the mild weather, weakening European demand, and lack of LNG demand in Asia in which the Japan/Korea Marker (JKM) average price during the first quarter of 2023 was at $18.06/MMBtu. EIA expects Henry Hub prices to average $2.65/MMBtu for the year's second quarter, unchanged from the Q1 2023 average. However, prices are expected to increase later in the year. European natural gas benchmarks TTF and JKM are expected to fall during Q2 2023 and grow during the second half of the year.

Source: EIA (U.S. Energy Information Administration)

The first quarter of 2023 has been challenging for the global oil market, with complex market dynamics and uncertainties such as the reversal of China's zero-COVID policy and the EU’s new sanctions on Russian-refined petroleum product exports, resulting in an increasing dislocation in the global oil trade.

The re-opening of China's economy has led to a surge in demand for oil products, particularly gasoline and diesel. This is due to stronger-than-expected air travel recovery, as people took advantage of the Lunar New Year holiday, and a large volume of road traffic which was 86% higher than during the same period in 2022. However, the pace and sustainability of this recovery still need to be determined. The IEA’s executive director, Fatih Birol, said in an interview with Bloomberg Television during this year's World Economic Forum that China presented the most significant uncertainty. “When I look at the markets, this year, 2023, there are many, many uncertainties. But if you ask me, which is the biggest uncertainty, I would say it is China … last year, 2022, for the first time since 40 years, Chinese oil and gas demand declined. … This year, the Chinese economy is reopening … and if Chinese demand for oil is strong, it will put upward pressure on prices.”

Furthermore, the EU agreed on two price caps for Russian petroleum products in February. The first price cap for petroleum products traded at a discount to crude oil is set at $45 per barrel, while the second price cap for petroleum products traded at a premium to crude is set at $100 per barrel. The G7 was due in mid-March to revise the price cap put in place in December but was eventually held off. On the other hand, willing buyers in Asia, particularly India and China, have been snapping up discounted crude oil cargoes. In February, Russia accounted for approximately 40% and 20% of Indian and Chinese crude imports, respectively. While Russian crude oil shipments are almost exclusively heading to Asia, a more diverse set of buyers for products backed out of the EU is emerging. It remains to be seen if there will be a sufficient appetite for Russian oil products now that the price cap is in place, or if production will start to fall under the weight of sanctions.

Global economic growth is expected to continue in 2023, with OECD economies supported by healthy consumption and investment and emerging economies like China and India showing promising growth prospects. Additionally, Russia may face challenges, but robust commodity markets, structural reforms, and fiscal support measures underpin their economies. A stable global oil market, thanks to successful cooperation efforts, will also provide ample oil supply to fuel economic growth.

While this projected economic growth is viewed as steady, there are both upside potential and downside risks to consider. Positive outcomes could arise from the US Federal Reserve effectively controlling inflation and the Eurozone exceeding its anticipated performance. Conversely, there are potential risks associated with current monetary policies and future measures that could affect global debt markets, resulting in a slowdown of economic growth. Additionally, persistent geopolitical tensions in Eastern Europe could also worsen the downsides. OPEC revised its forecasts in its March report, indicating a likely drop in global oil demand in Q2 compared to Q1. Moreover, the EIA expects a fall in the Brent Crude Oil spot price from an average of $84 per barrel in the second quarter of 2023 to $81 per barrel in Q4 and then an average of $78 per barrel in 2024.

December 31st, 2022 marked the kick-off of the EU taxation on windfall profits for fossil fuels producers and refineries, linked to the surge in energy prices following the war in Ukraine. The taxation will be applied on 75% of taxable profits from 2022 and 2023, which are more than 20% above the baseline from 2018 to 2021, in addition to the regular taxes and levies applicable in each EU member state country.

Adopted at the end of September 2022 by the EU Member States, this mandatory measure dubbed “temporary solidarity contribution” targets profits earned by companies generating at least 75% turnover in extraction, mining, refining of petroleum or manufacture of coke oven products. The regulation enabled the EU to levy 33% of the taxable profits of these multinationals in 2022, which could allow Brussels to recover 25 billion euros. Proceeds from these measures will be collected in September of this year and next year. They will then be redistributed to households and companies suffering from the impact of high retail electricity prices.

Some EU countries took the measure further, such as Romania, which more than doubled the size of the tax making it 60%, which prompted protests by industry associations and investors in the country. The British government also announced in November 2022 that a similar tax on profits from oil and gas drilling in the North Sea would increase from 25% to 35% and be extended for three years until 2028. In this context, Shell, the Anglo-Dutch energy company, has announced that it will pay "around $2 billion" in windfall profits to the European Union and the United Kingdom. Former Shell CEO Ben van Beurden, whom Wael Sawan replaced on January 1st, said that a more outstanding contribution from the sector to protect the households hardest hit by the energy crisis was "a social reality" that had to be "accepted.”

On the other hand, some of the affected companies are expressing their dissatisfaction with the new taxation, with ExxonMobil, which reported a record profit of 20 billion euros in Q3 2022, appealing with the Court of Justice of the European Union to challenge the tax adoption procedure as the EU 27 member states have resorted to an emergency text, which allows them to adopt a provision without involving the European Parliament. ExxonMobil also argues that the tax is counterproductive and will erode investor confidence. In early December, the company's financial director estimated the group's cost to be over 2 billion euros.

Global natural gas prices remained on a downward trend during the first quarter of 2023, primarily because of the persistent influx of LNG, sufficient gas storage inventories, and an unseasonably mild winter in the Northern Hemisphere. Moreover, the recovery of Asian demand was not as much as the market expected. These factors put pressure on the spot prices in Europe and Asia.

LNG imports into Europe continued at a high pace in Q1. Also, despite the Russian pipeline supply being gone, Europe has managed to escape winter with storage levels far higher than the average of the last five years. This result wouldn’t have been achieved without critical factors in demand. Europe managed to keep demand much lower than previous years, since, beyond the 15% reduction imposed by the EU, the actual numbers showed a more than 20% fall in gas consumption in the region.

As for the upcoming months of 2023, China's gas consumption is projected to see almost a 7% rebound, particularly in the industrial sector, thanks to the recovery of economic activity following the easing of Covid-19 restrictions and the country's newly signed LNG contracts. These contracts offer LNG at a lower average price than recent prices on the spot market. Furthermore, Russia's steep gas supply cuts to the European Union have put unprecedented pressure on European and global gas markets. The IEA predicts that assuming Russian gas supplies to Europe continue at their current level, Russian piped gas deliveries to OECD Europe will drop by almost 40% (or 30 bcm) in 2023 compared to 2022.

The uncertainty around the profile of Russian piped gas supplies could lead to a complete cessation of deliveries, putting further pressure on markets. The IEA also highlights that flexible LNG played a crucial role in partially offsetting the shortfall in Russian gas deliveries and maintaining gas supply security in Europe. Global flexible LNG imports are expected to increase by close to 7%, although a more robust recovery in China's LNG imports could limit this growth to just 3%.

At the end of March 2023, the 27 Energy Ministers of the European Union gathered in Brussels for a Council meeting, where they adopted the "gas package." This legislative package aims to reform the gas market and infrastructure in line with the Union's climate transition objectives. It consists of two legislative texts, a directive and a regulation, designed to facilitate the adoption of renewable and low-carbon gases, including hydrogen and biomethane. The primary objective of the European MEPs is to ensure that sufficient cross-border capacity is available to set up an integrated European hydrogen market, known as the "basic hydrogen infrastructure," to meet the REPowerEU targets.

The MEPs have proposed that member states collectively guarantee at least 35 billion cubic meters of sustainable biomethane production and injection into the natural gas system every year, intending to replace 20% of Russian natural gas imports with a sustainable, cheaper, and locally produced alternative by the end of 2030. To achieve this, the European Network of Gas Transmission System Operators (ENTSOG) may also require reform in order to cover hydrogen system operators.

The amendments also include a mechanism for member states to coordinate gas purchases, which was initially put in place under an emergency procedure. MEPs want EU countries to phase out fossil gas as soon as possible, considering the availability of alternatives. Member states may decide on an earlier end date for the duration of long-term fossil gas contracts without mitigation before the end of 2049.

A rebound in commodity prices caused by long-term geopolitical supply disruptions makes energy the best-performing sector in the large cap index of major US stocks. Operating free cash flows of North American exploration and production companies surpassed $83 billion in 2022, with a year-end cash balance of $70 to $100 billion. Additionally, oil and gas groups have paid off tens of billions of dollars in debt over the past year and have enough buying power to close deals while attracting renewed interest in mergers and acquisitions.

A few significant transactions were made in the first quarter of 2023, totaling $5 billion in January. These transactions included Diamondbacks and Marathon Oil, each paying $3 billion to acquire land in the Permian and Eagle Ford basins, Matador Resources' $1.6 billion buyout of a Permian driller backed by private equity fund "Advance Energy," and Vitol outbidding numerous major players to acquire privately held Delaware Basin Resources. Also, rumors of potential strategic deals have been circulating, with Pioneer Natural Resources eyeing resources in the CRR range for a possible acquisition.

According to the Financial Times, public and private players are becoming more inclined to sell. Private equity groups have already initiated a first round of fundraising while aiming to sell their assets with lucrative exit multiples. Furthermore, US oil and gas companies are gearing up for initial public offerings (IPOs), sending a strong signal to Wall Street investors. Notably, TXO Energy Partners became the first energy company to go public in over six months, and nine other energy companies filed or updated their IPO documents in January 2023.

It is predicted that major US shale producers will aim to enhance their operational efficiency and returns by consolidating their positions in the most prolific basins, which could enable them to generate more than $120 billion in additional revenue in 2023. The sector is projected to maintain its focus on generating cash flows, with anticipated amounts ranging from $70 to $90 billion this year. This outlook is expected to remain unchanged, even if the oil price, as measured by the American benchmark index West Texas Intermediate (WTI), reaches $65 per barrel.

The prospect of market consolidation underscores the importance of regulation in curbing anticompetitive practices. The regulation regarding M&A should be followed closely in the upcoming months.