Carbon Accounting Management Platform Benchmark…

There are now over $146bn of SPAC deals looking for merger candidates. But executing a merger is not the end of the story—many SPAC deals have performed poorly post-merger.

What are the key factors in successful deals?

Are there specific factors that relate to a SPAC’s success post-business combination with their target company?

There are a multitude of factors that relate to SPAC deal success in completing a merger, such as redemption count, focus alignment, speed of closing, and sponsor concessions (1). But many deals perform poorly post merger, particularly after expiration of the lockup period when selling company shareholders can sell their shares. What makes for a successful deal, long term?

The size of a deal can be an indicator of its eventual success. Over the past four years, deals with an enterprise value post-business combination of $2bn or more traded significantly better than smaller deals (1).

When evaluating an appropriate target company, SPACs generally will look to acquire a target that is at least three to five times the size of the SPAC trust account (2). The main purpose for this multiple is to mitigate the many forms of dilution of founder shares, the biggest of which is the sponsor “promote”, typically 20% (3).

Size is relative, and a key metric to put size into perspective is each SPAC deal’s Enterprise Value/Trust Multiple, which is the size of the acquired business relative to the SPAC’s trust account. Although a high EV/Trust Multiple isn’t predictable of ultimate success, three of the most successful SPAC deals as of July 2020 (QuantumScape, Draftkings and Iridium) had an EV/Trust Multiple between 800%-1800%, whereas most of the deals from 2016-2020 ranged from 200%-600%. A larger EV/Trust Multiple has tended to result in a higher stock price at the time of closing. This can be seen in the following chart.

“The primary source of SPACs’ high cost and poor post-merger performance is dilution built into the circuitous two-year route they take to bringing a company public. Along the way, SPACs give shares, warrants, and rights to parties that do not contribute cash to the eventual merger” (3).

While SPAC investors typically bear the costs and Sponsors receive astonishing returns, the long-term performance of the newcos has been shaky at best. As most SPACs value their shares at $10 when the merger takes place, but by time the business combination takes place, the average SPAC holds cash of just $6.67 per share (3). Over one-third of SPACs evaluated between January 2019 and June 2020 had redemptions over 90% with an average redemption rate of 58% (3). Since redemptions are at the issuance price of $10, compared to say $6.67 per share actually in the trust account, each redemption further dilutes the remaining shareholders. While the cash lost on these redemptions may be replenished by PIPE (Private investment in Public Entity) investors, the replacement is usually not in full and therefore the shares are yet further diluted, leading to the potential of diminished returns.

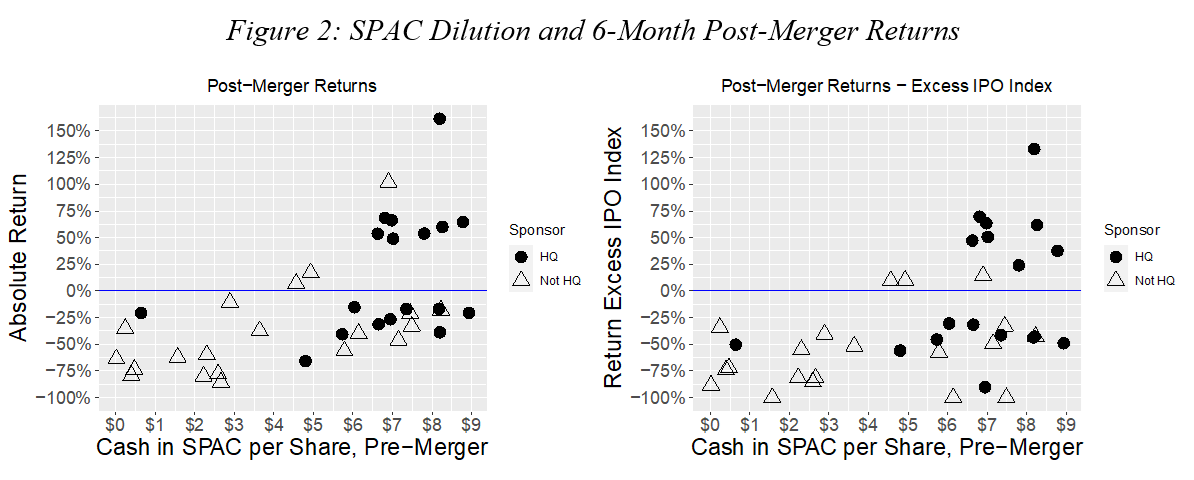

Obviously, the greater the dilution, the less cash is available in the trust account at the merger date, compared to the $10 issuance (and redemption) price. And unsurprisingly, high dilution deals perform poorly post merger, and low dilution deals perform relatively well. This graph (3) shows a high correlation between dilution and stock price performance. SPACs with lower cash per share at the merger date see larger post merger price declines. The most successful deals all have relatively small dilution: cash per share at the merger date of $7 per share or more.

Contributing to poor post merger performance has been a flood of secondary market buying and selling in SPACs, similar to the recent GameStop trading frenzy. SPACs have a large presence of short-term investors who look for opportunities to sell their shares shortly after business combination instead of taking a more long-term, fundamental approach.

And of course, once the lockup period expires, 180 days post merger, selling company shareholders are free to sell their shares as well.

The success of SPAC deal can also come from the management teams behind them, their expertise, and popularity. An analysis on 36 SPACs from 2015-2019 indicated that operator-led SPACs outperformed other SPACs by 40% and their sectors by 10%. “Operator-led” refers to a SPAC in which their Chairman or CEO has former C-suite operating experience. These operators can efficiently select sectors and target companies, while also taking on more responsibility for the success post-merger (4). For example, Kensington Capital’s SPAC, which merged with QuantumScape, the successful electric-vehicle battery maker, assembled a board of directors including former automotive executives (5).

The business expertise in operator-led SPACs may be enhanced by high-profile investors taking on the Sponsor role and leveraging their reputations and popularity to raise funds for their SPACs.

This graph (3) illustrates superior performance of SPACs run by private equity firms with greater than one billion dollars of assets under management or former Fortune 500 executives (referred to as “high-quality” or “HQ” deals). HQ SPACs had on average lower dilution (cash per share at the merger date averaging around $7 per share) and produced higher six-month post-merger returns for SPAC shareholders than Not HQ deals: 12-month returns for HQ SPACs showed a mean return of -6.0% whereas Not HQ SPACs are drastically lower at -57.3% (3). Furthermore, all the most successful deals were HQ deals.

“When commentators say SPACs are a cheap way to go public, they are right, but only because SPAC investors are bearing the cost.” (3) A major factor in SPAC dilution and poor performance is the “promote”, typically 20% of the stock issued to the Sponsor for a nominal consideration. The Sponsor gets paid the “promote” if the merger deal closes, irrespective of subsequent stock price performance. In addition, the Sponsor gets warrants, which give substantial upside if the deal is a success.

For example, one Goldman Sachs SPAC paid $16 million for warrants to acquire 8 million shares at $11.50 per share and received 20% of the company for a mere $5,000. That $5,000 investment may end up resulting in a $140 million payday upon merger completion. Another example is Third Point’s 2018 sponsoring of Far Point Acquisition Corp. Third Point raised $500 million and paid $12 million for warrants to buy 8 million shares at $11.50. They also received 20% of their founders shares for only $25,000. This investment will provide Third Point $100 million of their shareholder’s investment, regardless of success.

In many cases, Sponsors have had to give up some of their compensation, to attract “PIPE” (private investment in public equity) investors sufficient to finance the merger.

Research has shown that deals, where the Sponsor has been willing to sacrifice some of their promote, have traded better than deals in which the Sponsor has held onto the entire amount (6).

A number of alternative deal structures are being tried out by Sponsors and brokerage firms to better align sponsor and investor incentives:

Morgan Stanley has created a SPAC model called stakeholder aligned initial listing or “SAIL.” This method structures SPAC sponsors will only receive their promote shares if the merged company’s stock appreciates over time. This model has already translated to several deals, including CBRE Group Inc’s. SPAC, which raised over $400 million in December 2020.

Evercore has also created a new model, which they call “CAPS” (capital which aligns and partners with a sponsor). In this model, the sponsors receive 5% of the promote and after are paid 20% of the appreciation of the volume weighted average price of the stock (7).

Most notably, Bill Ackman and Pershing Square re-wrote their newest SPAC, Pershing Square Tontine Holdings (ticker: PSTH), a $4bn deal, to achieve better balance of incentives between Sponsors and end investors. Whereas virtually all SPACs have detachable warrants, PSTH warrants are two-thirds not detachable. This reduces the possibility of the investor to trade them as separate securities (which benefits short-term arbitrage investors) thus encouraging long-term holdings. In addition, investors do not even receive these two-thirds of warrants if they redeem their stock prior to the closing of the business combination.

To mitigate the disparity between investor and Sponsor returns, PSTH has taken steps to re-structure their compensation terms. PSTH paid $67.8 million for warrants to only acquire 6.21% of the company, compared to Goldman’s $16 million for 9.1% and Third Point’s $12 million for 12.8% of shares received. PSTH’s warrants are exercisable at a 20% premium versus Goldman Sachs’ and Third Point’s 15% and will not exercise for three years after closing the acquisition, further facilitating their long-term investing approach (8).

The structure of PSTH has served as a benchmark for other SPACs to follow suit. Starboard Value Acquisition Corp (ticker: SVAC), raised over $360 million in their IPO and sold investors one-sixth of a warrant, plus the right to receive another one-sixth if they do not redeem when a merger is announced. While investors still have the option to redeem if they do not agree with the merger, this similar action to PSTH promotes long-term growth and incentivizes investors to stick with the company post merger. While no SPAC to date has followed suit of PSTH with no promote, Ribbit Leap Ltd. (ticker: LEAP) raised $350 million where founders will receive 10% of the post merger shares and additional shares if performance thresholds are met. In addition, Executive Network Partnering Corp. (ticker: ENPC), led by former U.S House Speaker, Paul Ryan, has granted sponsors 5% of shares with the ability to acquire an additional 15% if the stock rises 10% from IPO pricing post merger (9).

So, what is next for SPACs in 2021? Much of the foregoing analysis is based on historic, completed SPAC deals. However, over 82% of the 478 SPAC deals done in 2020 and 2021 (as of March 12, 2021) are uncompleted and have yet to identify a target. Uncompleted deals amount to over $146 billion, with more money being raised every week (10).

There are clearly key factors which improve the probability of long-term success of SPAC deals, including EV/Trust multiples, quality of sponsors and management, and deal structure, as well as other factors, including dilution and compensation, which negatively impact the probability of success. Alternative deal structures such as PSTH promise better alignment of incentives between Sponsors and end investors, but it remains to be seen whether these structures take a major share of the market, and whether the eventual mergers resulting from these structures are themselves successful.

As all these uncompleted deals look for merger candidates, as Sponsors and broker-dealers compete for new business and investor funds, and as regulators look in more detail at the growth of the SPAC market, there will be plenty of changes in the coming year.

John Gustav

Partner

+ 1 (516) 810 8719

John.Gustav@sia-partners.com

Danielle Fair

Manager

+1 (267) 614 2730

Danielle.fair@sia-partners.com

Joseph Willing

Managing Director

+1 (347) 380 3960

Joseph.Willing@sia-partners.com

McKinsey- Earning the premium: a recipe for long-term SPAC success

Bill Ackman and Tontine Holdings rewrite the terms for SPACs

{kind=link}

{kind=link}

{kind=link}