Carbon Accounting Management Platform Benchmark…

As a function of the European Green Deal, existing regulations closely correlated to the NFRD-SFDR-Taxonomy triptych will be amended.

The EU has made it a priority to improve its regulatory arsenal so that all financial market players take ESG criteria into account: first and foremost, investors, but also insurance companies, banks, investment firms and benchmark administrators. Designing a reliable regulatory framework for ESG criteria is not only a guarantee of sovereignty and consistency, but also international credibility; it is highly likely that the EU will strengthen its leading position in green finance with the advent of a regulatory standard for green bonds.

The Directive and Regulation on Markets in Financial Instruments are regarded as the cornerstone of the EU regulation of financial markets, aiming for transparent, integrated, and competitive financial markets. To strengthen investor protection, MiFID/R previously introduced strong requirements on reporting, product governance, disclosure to clients, independence of advice, and inducements. As part of its Sustainable Finance agenda, the European Commission now plans to amend MIFID II to enhance the existing legislative framework (notably SFDR and Taxonomy) and integrate sustainability considerations into the investment, advisory and disclosure processes in a coherent way within the financial system.

If adopted, this review could bring far-reaching changes for investment firms. Investment firms are currently required to obtain information on the profile, knowledge, experience, and financial objectives of their clients under the current MiFID/R framework. Going forward, they will have to include the non-financial objectives of their clients in their selection process (especially their sustainability preferences) and consider ESG criteria within their own portfolio management. To do so, the European Commission integrated recommendations on organisational requirements prepared and publicly consulted by ESMA into the draft delegated regulation. Finally, investment firms will have to integrate ESG factors and risks into all their processes, meaning that they will have to provide additional information to ESMA and investors. This will inevitably lead to higher compliance costs for investment firms.

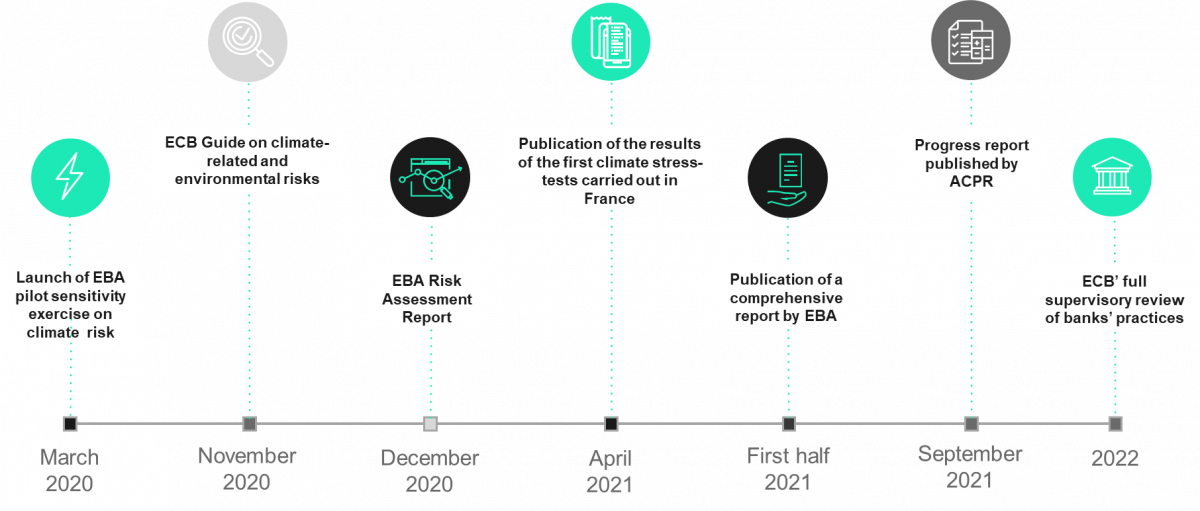

Since the subprime crisis, the EBA initiated stress tests, in cooperation with the national competent authorities (NCAs), the European Central Bank (ECB) and the European Systemic Risk Board (ESRB), to ensure that the banking system is adequately capitalized and can withstand macroeconomic and financial shocks. In line with the EU's regulatory corpus for sustainable finance, on November 27th, 2020, the ECB published a non-binding Guide on climate-related and environmental risks, so that institutions integrate these risks into their strategy, business objectives and risk management framework in the short, medium or long term. In early 2021, significant institutions are expected to use this Guide and conduct a self-assessment on ECB expectations, while smaller institutions are only invited to do so.

The first objective is to assess the sensitivity of institutions to climatic risks. The ECB expects institutions to monitor, on an ongoing basis, the impacts of climate-related and environmental factors on their current market risk positions and future investments, and to develop stress tests that incorporate climate-related and environmental risks.

The second objective will consist of analysing the difficulties encountered by institutions in conducting this type of exercise. Indeed, the Guide will serve as a basis for supervisory dialogue between the ECB and institutions, meaning that the legislation may be amended according to possible divergences with the institutions' practices.

In parallel to the ECB exercise, the results of the first climate stress-tests carried out in France in 2020 will be published in April 2021 so that an initial progress report can be made at the ACPR, the French Prudential Supervision and Resolution Authority at the end of September 2021.

It is important to note that climate risk is not explicitly considered in the adverse scenario as methodologies still need to be developed to integrate it into a stress test regulatory framework. Moreover, EBA is currently carrying out a pilot sensitivity study on a sample of volunteering banks which consists in measuring EU corporate exposures in relation to climate risk. Though preliminary results of the exercise have already been published, a more detailed and comprehensive report is expected in the first half of 2021. The ECB will then conduct a full supervisory review of banks’ practices in 2022 and take concrete follow-up measures where needed.

Benchmark Regulation was applied from January 1st, 2018 and originally applied to mainstream indices and financial instruments. Its main purpose was to address concerns about the accuracy and integrity of benchmarks, which were exacerbated by the Libor and Euribor scandals. At that time, Benchmark Regulation intended to improve the governance and controls of the benchmark’s evaluation process, and to improve the quality of data and methodologies. Thus, when it came into force, it already introduced requirements for benchmarking administrators, data providers and users of benchmarks, but ESG and sustainability were not original benchmark factors, and this must change.

The amended Benchmark Regulation, which entered into force on April 30th, 2020, closes this gap by introducing two types of climate reference benchmarks: the EU Climate Transition Benchmark and the EU Paris-aligned Benchmark. In order to label benchmarks as EU Climate benchmarks, minimal technical requirements should be respected. This regulation also proposes comparable standards for the methodology for benchmarking low-carbon performance in the EU, while allowing administrators a certain level of flexibility. Similar to SFDR, the Benchmark Regulation fights against greenwashing.

The EU Green Bond Standard was announced in the European Green Deal Investment Plan of January 14th, 2020. It is not yet in effect, but it should reinforce the role of green bonds in financing the assets needed for the green transition. Through standardization, the EU GBS could also strengthen the international role of the euro (the main currency for green bond issuances) and turn the EU into the global centre of green finance.

Nevertheless, the European Commission’s Inception Impact Assessment, which is based on the TEG recommendations, highlighted some hurdles such as the lack of definition as to what “Green” is, the complexity of green bond review procedures, the lack of 'investable' projects, and its higher issuance cost compared to a standard bond issuance. While some expect it to be used as a basis for other sustainable products (Green Loans, Social Bonds), there is currently no certainty around the mechanics. Indeed, the European Commission has cautiously scheduled the next deadline of Q1 2021 as an indicative timeframe after launching a targeted consultation.

All these regulatory changes are (or will be) both opportunities and constraints for financial institutions, which will have to comply with more disclosure and information obligations overall. These financial institutions will therefore have to bear additional costs to comply with applicable legislation and, particularly, to access reliable ESG data. The regulatory burden and associated costs are not the only issues that are singled out: all stakeholders deplore the growing dependence on non-European data providers and urge the European legislator to counter this trend, either through regulatory initiatives (including a review of the conditions necessary for granting equivalence decisions and their content) or by further promoting European data providers.